How Central Bank Interest Rates Move Stock Markets: The Direct Transmission Mechanism

DSIJ Intelligence / 26 May 2026 / Categories: Knowledge, Trending

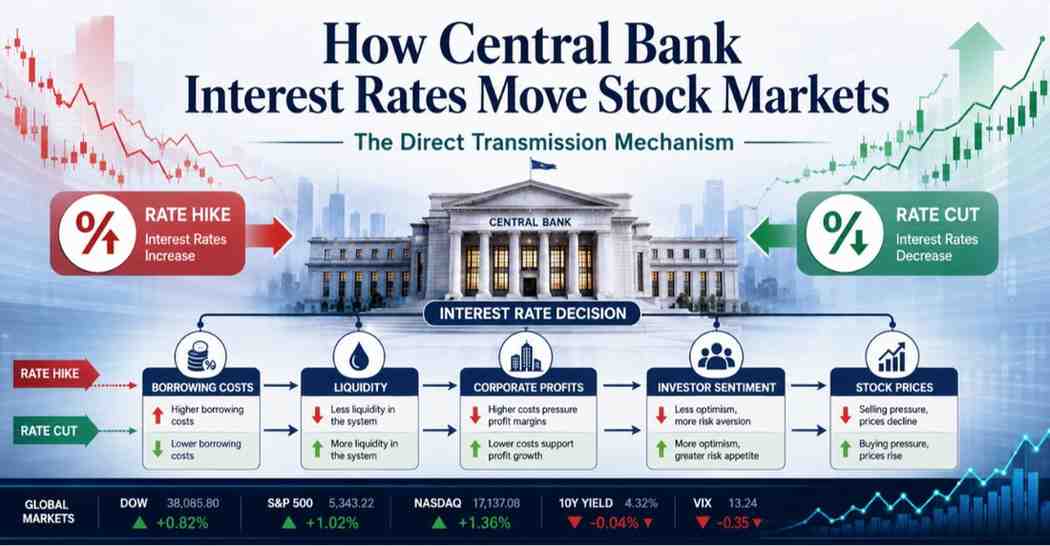

How repo rate decisions influence borrowing costs, corporate earnings, investor sentiment and stock valuations.

Whenever the head of a central Bank, like the Governor of the Reserve Bank of India (RBI) or the Chair of the US Federal Reserve, steps up to a microphone to announce an interest rate decision, Wall Street and Dalal Street collectively hold their breath.

If the central bank announces a "rate hike" (increasing the benchmark interest rate), stock markets often tumble. Conversely, when interest rates are cut, markets frequently celebrate with a massive rally. But why does a small change in a banking number affect the value of a tech company, a car manufacturer, or a retail chain? The connection is not random; it is driven by a highly logical machine called the direct transmission mechanism.

Here is exactly how a change in interest rates ripples through the economy and directly changes what a stock is worth.

The Ultimate Gravity: The Cost of Capital

To understand how interest rates move stocks, think of interest rates as economic gravity. When gravity is low (low interest rates), everything can float effortlessly upward. When gravity is high (high interest rates), pulling things off the ground becomes much harder.

The primary rate set by a central bank (known as the Repo Rate in India) is the interest rate at which commercial banks borrow money from the central bank.

- Step 1: Central bank hikes rates.

- Step 2: Commercial banks raise lending rates.

- Step 3: Higher borrowing costs for businesses and consumers.

When the central bank hikes this rate, it becomes more expensive for your local bank to source money. To protect their profit margins, commercial banks immediately pass this cost down to everyone else by raising interest rates on home loans, car loans, and business loans.

Path 1: Corporate Earnings Under Pressure

The first direct hit from a rate hike lands squarely on a company's financial statements. Most companies rely on debt to fuel their operations, build new factories, or fund research.

A Simple Example: The ABC Car Company

Imagine a large automobile company called ABC Car Company.

- ABC Cars has RS 1,000 crore in floating-rate corporate loans that it used to build its automated assembly lines.

- If the central bank raises interest rates by 1 per cent, the interest rate on ABC Cars' loan might jump from 8 per cent to 9 per cent.

- Suddenly, ABC Cars must pay an extra RS 10 crore every year just to service its existing debt.

Because that extra RS 10 crore goes entirely to the bank to pay interest, it is completely wiped out from the company’s Net Profit. When profits fall, the company becomes fundamentally less valuable to investors, causing its stock price to decline.

Furthermore, higher rates squeeze ABC Cars from the consumer side, too. Because car loans are now more expensive, retail customers decide to defer purchasing a new vehicle. Demand drops, revenues shrink, and corporate earnings take a double hit.

Path 2: The Equity Valuation Model (The Discount Rate)

Even if a company has zero debt and robust sales, a rate hike will still lower its stock price. This happens because of a core mathematical financial concept: The Present Value of Money.

When equity analysts value a stock, they look at all the cash and profits the company is expected to make 5, 10, or 20 years into the future. They then "discount" those future profits back to today's terms to determine what the stock is worth right now. The interest rate forms the baseline for this discount rate.

The Golden Rule of Valuation: The higher the interest rate (discount rate) in an economy, the less valuable those future corporate earnings look to an investor today.

A Simple Analogy: The Bird in the Hand

Imagine someone promises to give you RS 10,000 exactly five years from today.

- If a guaranteed bank Fixed Deposit (FD) pays only 3 per cent interest, that future RS 10,000 looks highly attractive because parking cash in a bank yield very little. You would be willing to pay a high price today to secure that future cash.

- Now, if the central bank hikes rates and bank FDs suddenly offer a guaranteed 7.5 per cent interest, that future corporate payment looks much less appealing. Why risk your money on a company when a safe government bond or bank deposit offers a fantastic yield?

To compensate for this, investors demand a much cheaper entry price for the stock. This formulaic repricing happens automatically across thousands of algorithm-driven trading desks the second a rate hike is announced, causing equity valuations to compress across the board.

Path 3: The Realignment of Investor Capital

At its core, the stock market competes with the bond and fixed-income market for investor capital.

When central bank interest rates are rock bottom, safe investments like government bonds or savings accounts pay next to nothing. Investors looking to grow their wealth are practically forced to move their capital into the stock market to chase higher returns. This massive influx of money drives up stock demand and elevates market prices.

When a central bank hikes rates, the script flips completely. In a low-interest-rate environment, safe havens like FDs and bonds are highly unattractive due to low yields. This forces investors to shift capital into equities, resulting in higher stock valuations.

Conversely, in a high interest rate environment, safe havens provide high yields and become very attractive risk-free returns. Investors shift their capital out of equities and into bonds, leading to a stock market cooling and price drops.

For institutional asset managers overseeing billions, moving even 5 per cent or 10 per cent of their fund from volatile equities into newly high-yielding, risk-free government bonds pulls massive liquidity out of the stock market, resulting in downward pressure on stock indices.

The Silver Lining: Not All Sectors Are Equal

While a central bank rate hike acts as a general drag on the broader indices, the transmission mechanism affects different sectors in unique ways:

- Growth and Tech Stocks (Hardest Hit): Technology and startup-phase companies typically rely on earnings far out in the future. Because their biggest payday is years away, a higher discount rate severely shrinks their current valuation.

- Banking and Financials (Often Benefit): Commercial banks can actually experience expanded profit margins during early rate-hike cycles. They are incredibly quick to raise lending rates on borrowers, while lagging behind in raising the interest rates they pay out to savers on deposit accounts.

Summary

Central bank interest rates are the steering wheel of the financial markets. A rate hike acts as an intentional brake on the economy. It dampens consumer spending, increases corporate debt costs, mathematically reduces what future corporate profits are worth today, and coaxes conservative investor money out of stocks and into safe-haven bank accounts. Understanding this direct machinery allows investors to look past day-to-day market panic and evaluate businesses with clarity and long-term perspective.

Disclaimer: The article is for informational purposes only and not investment advice.