Welspun Corp Has Doubled From Its 52-Week Low. The Market May Be Pricing More Than Just a Good Quarter

A record order book, visible earnings growth, strong US demand for line pipes, new capacities nearing commissioning in Saudi Arabia and the United States, and a balance sheet that remained net cash despite Rs 2,532 crore of capex have all strengthened the case for Welspun Corp. The stock’s 75% rally in three months increasingly looks like a reassessment of the business rather than just a reaction to one quarter’s earnings

✨ મુખ્ય મુદ્દાઓ

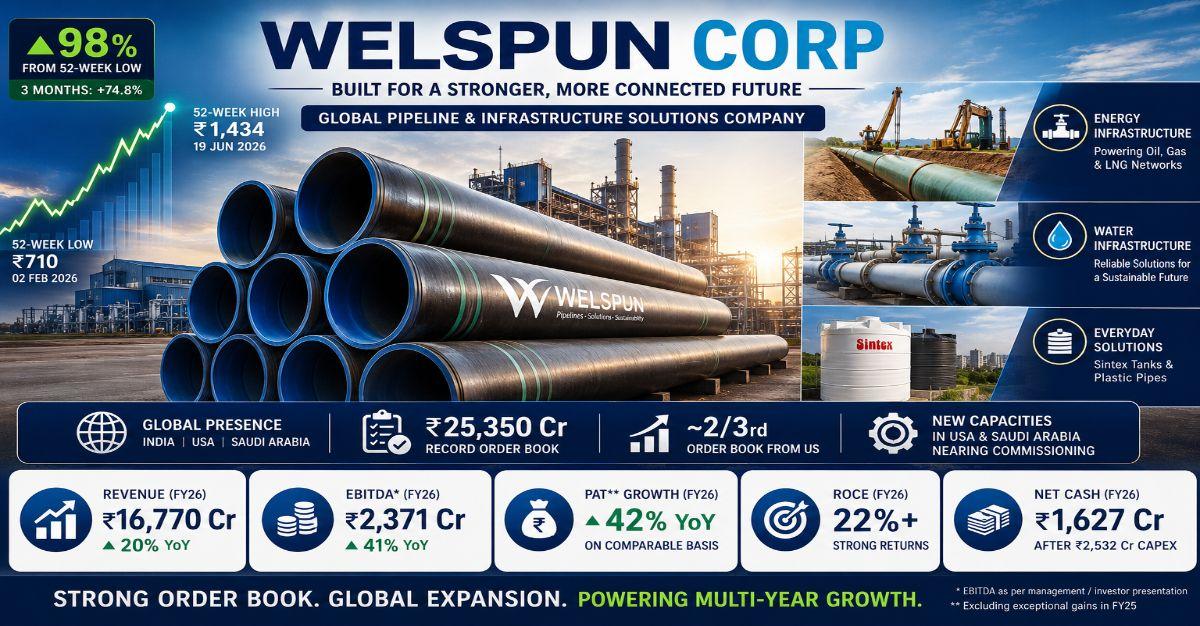

Welspun Corp hit a 52-week high of Rs 1,434.3 on June 19, 2026. The stock currently trades near Rs 1,405, up almost 98 per cent from its 52-week low of Rs 710 hit on February 2, 2026. Over three months, the stock has returned 74.8 per cent. Over one year, it is up 53.5 per cent. Over three years, it has returned 424 per cent, while five-year and ten-year returns stand at 836 per cent and 1,573 per cent, respectively.

Moves of that magnitude usually reflect more than a single quarter’s earnings surprise. In Welspun Corp’s case, the market appears to be reassessing a business that has become broader, more profitable and more globally diversified than it was a few years ago.

What the business looks like now

Welspun Corp is often still viewed primarily as an Indian pipe manufacturer tied to lumpy domestic infrastructure and energy orders. That description is no longer sufficient.

The company now operates across four meaningful business pillars: large-diameter line pipes used in oil and gas transmission, ductile iron pipes used in water distribution, Sintex water tanks and plastic pipes, and Welspun Specialty Solutions, which manufactures stainless steel products. Its operating footprint spans India, the United States and Saudi Arabia, while its Order Book is increasingly driven by international opportunities. Management has indicated that around two-thirds of the current order book is linked to the US market.

That shift matters because it changes how the business should be viewed. Welspun is no longer only a domestic pipe player dependent on the timing of Indian project awards. It is increasingly a broader pipeline and water infrastructure platform with exposure to global energy and water capex cycles.

The FY26 numbers that changed the conversation

Welspun’s FY26 financial performance gave the market a much clearer picture of the underlying earnings trajectory. Revenue rose to Rs 16,770 crore in FY26 from Rs 13,978 crore in FY25, reflecting 20 per cent growth. EBITDA, as indicated by management and the investor presentation, increased from Rs 1,684 crore to Rs 2,371 crore, translating into 41 per cent growth. Profit after Tax is best viewed on a comparable basis because FY25 included large exceptional gains, including the Nauyaan Shipyard stake sale and the EPIC stake sale. On management’s adjusted basis excluding these exceptional items, FY26 PAT grew 42 per cent year-on-year. The company also delivered ROCE of more than 22 per cent in FY26 and closed the year with an order book of Rs 25,350 crore, underlining both profitability and revenue visibility.

The PAT comparison is important. On the surface, reported profit growth can look less straightforward because FY25 included one-off gains. But once those exceptional items are stripped out, the underlying picture is clearer: revenue grew 20 per cent, EBITDA rose sharply and profitability improved meaningfully.

Management has guided for FY27 revenue of around Rs 20,000 crore and EBITDA of around Rs 2,850 crore. That implies another year of high-teen growth in both revenue and EBITDA. More importantly, it suggests that FY26 may not have been a peak year but part of a broader earnings upcycle.

Why the US business matters more than before

A key reason for the recent rerating appears to be the market’s changing view of Welspun’s US opportunity. Earlier, the US business may have been seen largely as a cyclical export-driven opportunity. Management commentary now points to a broader and more durable demand environment.

The first demand driver is LNG-linked gas infrastructure. US natural gas prices remain structurally lower than international LNG prices, which continues to support investment in gas transportation infrastructure linked to export facilities.

The second is the possibility of incremental pipeline demand tied to data centre-led power investments. Management indicated that the rapid buildout of data centres in the US could support demand for gas-based power infrastructure, which in turn may require additional pipeline connectivity. This is still an emerging part of the story, but it adds another layer to the US opportunity beyond traditional oil and gas transportation.

The third driver is renewed investment in oil pipeline infrastructure, which management believes is also contributing to demand.

Taken together, these factors suggest the US business is no longer just about a few export orders. It may now be part of a broader multi-year energy infrastructure cycle, which helps explain why the market is assigning greater value to Welspun’s order book and capacity expansion plans.

Saudi Arabia could become the next growth leg

Welspun’s investments in Saudi Arabia are another important part of the story. The company has set up large-diameter pipe and ductile iron pipe capacities in the region, and management has indicated that these assets should begin contributing from FY27, with fuller benefits likely visible in FY28.

The significance of Saudi Arabia is not limited to oil and gas. The region is also investing in water transmission and distribution infrastructure, which creates demand for both large-diameter pipes and ductile iron pipes. That broadens the opportunity set and gives Welspun a presence in a market where water infrastructure and industrial development are likely to remain key spending priorities.

For investors, the important point is that Welspun’s recent capex cycle is now moving closer to the monetisation phase. As these capacities begin to contribute, the market is starting to look beyond the capex outflow and focus more on the earnings potential they can create over the next two years.

A balance sheet that strengthens the growth story

One of the more impressive aspects of Welspun’s FY26 performance is that it funded a large capex programme without weakening the balance sheet.

The company spent Rs 2,532 crore in capex during FY26 and still ended the year with a net cash position of Rs 1,627 crore. Operating cash flow stood at Rs 3,204 crore, while free cash flow remained positive at around Rs 715 crore. Debt-to-equity stood at 0.26 and interest coverage at 11.1x.

That matters because industrial companies often face a trade-off between growth and balance-sheet quality. Welspun’s FY26 numbers suggest it was able to pursue expansion while still maintaining healthy cash generation and moderate leverage. Customer advances also supported working capital efficiency, which helped the company sustain cash flows through the capex cycle.

Why the stock had gone quiet before this breakout

The stock’s consolidation through much of CY25 and into early 2026 also fits the broader story.

First, headline profitability comparisons were made harder by the exceptional gains booked in FY25. That may have obscured the improvement in underlying profitability and delayed the market’s recognition of the earnings trend.

Second, the domestic business had seen some softer patches. Management acknowledged muted growth in parts of the Indian business and highlighted challenges in ductile iron pipes, including industry overcapacity and payment delays from state-linked projects. Those issues likely tempered sentiment for a period even as the international opportunity was improving.

Third, Welspun was in the middle of one of its heaviest capex phases, with investments underway in both the US and Saudi Arabia. During such periods, investors typically wait for greater clarity on commissioning timelines, capacity utilisation and the actual earnings contribution from new assets. FY26 results, FY27 guidance and management commentary appear to have provided more of that clarity.

The rerating is visible in valuation too

The stock’s valuation suggests the market is assigning a higher quality and visibility premium to the business than it did in the recent past.

Welspun currently trades at around 22.9x earnings, compared with its three-year median P/E of roughly 15.3x. That indicates a meaningful re-rating in the earnings multiple, in addition to the improvement in profits. At the same time, the stock is now trading broadly in line with the industry P/E of around 22.3x, suggesting that the market is no longer treating Welspun as a lower-quality cyclical pipe name.

EV/EBITDA of around 13.4x is also better read alongside the order book, return ratios and earnings visibility rather than in isolation. If the FY27 guidance is delivered and new capacities begin contributing on schedule, the current valuation could be seen as the market paying for a business with a stronger and more diversified earnings base than before. That said, the sharp rally also means a good part of the near-term optimism is now reflected in the stock price.

Risks the market should keep in mind

The first key risk is execution. The next phase of growth depends on the US and Saudi capacities ramping up on schedule and achieving utilisation levels that justify the capital deployed.

The second is order book conversion. A large order book provides visibility, but revenue recognition still depends on project timelines, customer execution and regulatory approvals.

The third is domestic ductile iron pipe demand. Industry overcapacity and payment delays in state-led projects remain important variables, especially if the domestic market takes longer to recover.

Finally, commodity costs, freight movements and geopolitical disruptions can still affect margins and execution, even if the company currently appears better positioned than in earlier cycles.

The core takeaway

Welspun Corp’s recent rally is best understood not as a one-quarter reaction, but as a broader reassesSMEnt of the business. The company has moved beyond being viewed as a cyclical domestic pipe manufacturer and is increasingly being valued as a global pipeline and water infrastructure player with a record order book, visible earnings growth, expanding international capacities and a balance sheet that has remained strong through a heavy capex cycle.

The stock’s consolidation through CY25 now looks like a phase in which the market was waiting for cleaner earnings visibility and greater clarity on the benefits of the capex programme. The breakout since February suggests that confidence has improved on both counts.

Disclaimer: This article is for informational purposes only and not investment advice.